The Key Partnerships That Enable Prepaid Programs

Prepaid products—in all forms from consumer products to business funded B2B products—are powered by a complex network of partnerships. If your organization sources prepaid cards you likely have a strong relationship with one or several program managers, but for those considering building their own program you often encounter a fragmented ecosystem. There are several critical relationships that make prepaid solutions possible, and I want to help you understand each player's role.

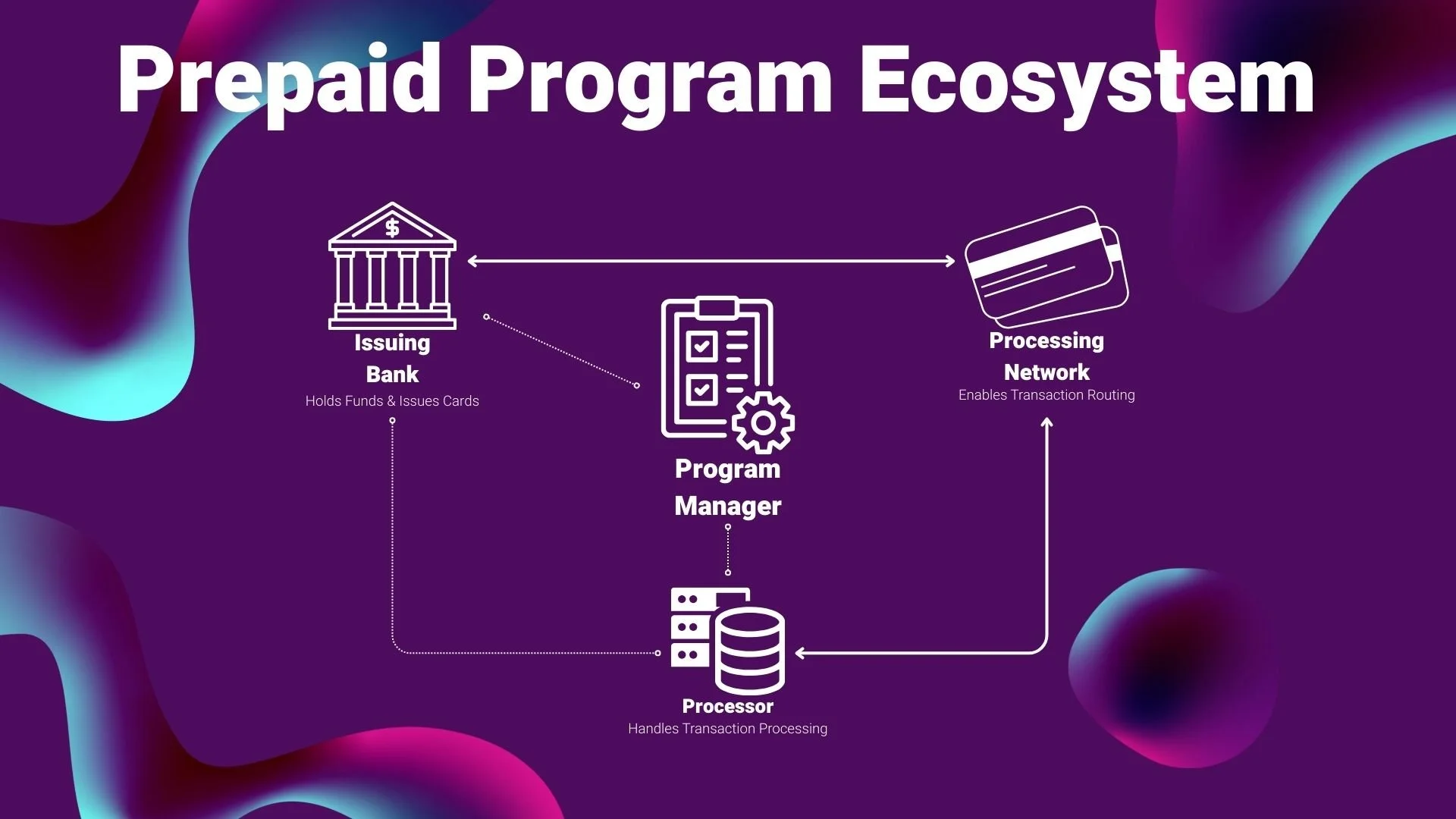

At the core of every prepaid program are four essential components: the issuing bank, the processing network, the processor, and the program manager. Each plays a distinct role in ensuring regulatory compliance, transaction processing, and program execution. I’m going to help you break down these components, explore how they function, and discuss how the lines between them sometimes blur.

The Four Core Components of a Prepaid Program

1. Issuing Bank

The issuing bank is a regulated financial institution responsible for holding cardholder funds, issuing prepaid cards, and ensuring compliance with financial regulations. Because prepaid programs involve stored-value accounts, they must be backed by a licensed bank that has the authority to issue cards under a card network (e.g., Visa or Mastercard). The issuing bank also plays a role in risk management, regulatory oversight, and compliance with anti-money laundering (AML) and Know Your Customer (KYC) regulations, Bank Secrecy Act (BSA), and Regulation E (EFTA).

Key responsibilities:

Holds and safeguards cardholder funds

Issues prepaid cards under a card network’s license

Ensures compliance with banking regulations and network rules

Provides regulatory reporting

2. Processing Network

The processing network, commonly Visa, Mastercard, or another closed-loop provider, acts as the highway for transaction approvals and settlements. It enables the prepaid card to be accepted by merchants, ensuring transactions are authorized, processed, and settled in real time.

Key responsibilities:

Facilitates transaction authorization and settlement between issuing banks and merchant banks

Enforces network rules and security protocols

Provides global acceptance and merchant connectivity

3. Processor

The processor is the technological backbone of a prepaid program, handling transaction routing, approval/denial decisioning, cardholder balances, and system integrations. The processor works closely with the issuing bank and the network to ensure transactions are approved correctly and cardholders have real-time access to their funds.

Key responsibilities:

Maintains ledger and authorizes transactions

Connects with the issuing bank to update funds availability

Supports API integrations for program managers and enterprises

Provides fraud monitoring and risk management tools

4. Program Manager

The program manager’s chief responsibility is distribution. They are typically incentivized to sell the products. To do this they design, operate, and manage the prepaid product on behalf of the issuing bank and processor. This entity ensures the program meets business goals, integrates the necessary partners, and maintains compliance with regulatory and network requirements. A program manager typically handles customer support, dispute resolution, and operational oversight, making prepaid programs viable for business and consumer use cases.

Key responsibilities:

Designs and launches prepaid programs

Manages partnerships with banks, processors, and networks

Ensures compliance with industry regulations

Provides customer support and operational oversight

Where the Lines Blur

While these four components represent distinct functions, many organizations take on multiple roles. For example:

Some issuing banks also operate their own processing platforms, offering an all-in-one solution.

Certain program managers develop their own processing technology, reducing reliance on third-party processors.

Large fintech companies may serve as both a program manager and a licensed issuer, giving them more control over their prepaid programs.

Some card networks provide direct issuing and processing services, streamlining the entire value chain.

Adjusting these levers allows an organization to calibrate the amount of influence it has over the program. The more an organization consolidates these roles, the greater the control it has over pricing, compliance, and customer experience—but this comes with increased regulatory responsibilities and operational complexity. By outsourcing more of these responsibilities to partners an organization may be able to go to market quicker, but this tradeoff requires thoughtful, strategic relationships and management.

Summary

Understanding the partnerships that enable prepaid products is critical for organizations evaluating whether to source prepaid solutions or build their own program. The issuing bank, processing network, processor, and program manager each serve vital functions, and businesses must carefully assess which partnerships to engage in and how much control they want to retain.

For companies considering their own prepaid programs, the key is balancing control, cost, and complexity—leveraging partnerships where needed while ensuring they have the flexibility to scale efficiently.

By understanding these core roles and how they intersect, businesses can make informed decisions about how to structure their prepaid offerings and optimize their approach in the evolving payments landscape.